Starting retirement planning at 30 with no savings might feel overwhelming, but you’re not alone. Millions of Americans in their 30s face this exact challenge. The good news is that 30 is still young enough to build substantial retirement wealth through smart planning and consistent action. Learning how to start retirement planning at 30 with no savings is a critical step toward securing your financial future.

Moreover, your 30s represent a golden opportunity for retirement savings. You have decades of compound interest working in your favor. Additionally, you’re likely earning more than in your 20s, making it easier to allocate funds toward retirement accounts. Consequently, starting now—even from zero—can lead to a comfortable retirement if you follow proven strategies and maintain discipline throughout your journey.

Understanding Financial Planning Fundamentals in Your 30s

Financial planning in your 30s requires a strategic approach that balances current needs with future security. Furthermore, understanding core concepts like budgeting, debt management, and investing basics forms the foundation of successful retirement planning. Americans in their 30s often juggle multiple financial priorities, including student loans, mortgages, and family expenses.

Creating Your First Budget for Retirement Success

Building a realistic budget is the cornerstone of retirement planning for beginners. Start by tracking every expense for one month to understand where your money goes. Subsequently, categorize expenses into needs, wants, and savings. Most financial experts recommend the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Additionally, money management strategies can help you optimize your spending patterns and free up funds for retirement contributions.

For Americans starting from scratch, even contributing $100 per month to retirement accounts can grow significantly. For example, investing $100 monthly with a 7% annual return yields approximately $122,000 after 30 years. Therefore, starting small is infinitely better than not starting at all.

Eliminating Debt While Building Retirement Savings

Debt management is crucial when starting retirement planning at 30 with no savings. High-interest credit card debt can sabotage your retirement goals. However, you don’t need to be completely debt-free before saving for retirement. Instead, adopt a balanced approach that addresses both simultaneously.

Focus on paying off high-interest debt first while maintaining minimum payments on other obligations. Consequently, you can redirect those payments toward retirement accounts once the debt is eliminated. For instance, if you’re paying $200 monthly on credit card debt at 18% interest, eliminating that debt frees up $2,400 annually for retirement savings. Moreover, understanding what increases your total loan balance helps you avoid common pitfalls that can derail your financial progress.

Understanding Your Current Financial Position

Before creating a retirement plan, assess your current financial health honestly. Calculate your net worth by subtracting liabilities from assets. Furthermore, review your credit score, as it affects loan rates and insurance premiums. Understanding what is included in personal assets helps you accurately evaluate your starting position.

Additionally, identify your monthly cash flow—income minus expenses. This number determines how much you can realistically save for retirement. For many Americans in their 30s, unexpected expenses derail savings plans. Therefore, building an emergency fund alongside retirement savings provides essential financial security.

Retirement Account Options for Americans in Their 30s

The United States offers several tax-advantaged retirement account options that can accelerate your savings journey. Understanding each option’s benefits and limitations is essential for maximizing your retirement contributions.

401(k) Plans: Your Employer-Sponsored Solution

A 401(k) is often the best starting point for retirement planning at 30. These employer-sponsored plans offer significant advantages, including pre-tax contributions that reduce your taxable income. For 2025, employees can contribute up to $23,000 annually to their 401(k), with an additional $7,500 catch-up contribution allowed for those 50 and older.

Moreover, many employers offer matching contributions—essentially free money for your retirement. For example, if your employer matches 50% of your contributions up to 6% of your salary, contributing $3,000 annually yields an additional $1,500 from your employer. Consequently, always contribute at least enough to capture the full employer match. Additionally, setting up a 401k for small business owners provides similar benefits for self-employed individuals.

If your employer doesn’t offer a 401(k), consider a solo 401(k) for self-employed individuals. This option allows higher contribution limits because you contribute as both employer and employee. Furthermore, exploring 401k plans for small business options can help entrepreneurs build retirement wealth while managing their companies.

Traditional IRA vs. Roth IRA: Choosing Your Path

Individual Retirement Accounts (IRAs) provide another excellent avenue for retirement savings. The fundamental difference between Traditional and Roth IRAs lies in tax treatment. Traditional IRAs offer tax deductions now, with taxes paid upon withdrawal. Conversely, Roth IRAs use after-tax dollars but offer tax-free withdrawals in retirement.

For 2025, the IRA contribution limit is $7,000 annually, with an additional $1,000 catch-up contribution for those 50 and older. Americans in their 30s often benefit more from Roth IRAs because they’re typically in lower tax brackets than they’ll be in retirement. Additionally, Roth IRAs offer more flexibility, allowing penalty-free withdrawals of contributions (but not earnings) before retirement.

However, income limits apply to Roth IRA contributions. For 2025, single filers earning above $161,000 and married couples filing jointly earning above $240,000 face contribution restrictions. Therefore, high earners might consider backdoor Roth IRA conversions or focus on Traditional IRAs instead.

Health Savings Accounts: The Hidden Retirement Tool

Health Savings Accounts (HSAs) represent an often-overlooked retirement savings vehicle. Available to those with high-deductible health plans, HSAs offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For 2025, individuals can contribute $4,300 annually to an HSA, while families can contribute $8,550. Furthermore, unlike Flexible Spending Accounts (FSAs), HSA funds roll over annually and never expire. Consequently, you can invest HSA funds for long-term growth and use them for healthcare expenses in retirement.

Medical costs represent one of retirees’ largest expenses. Therefore, maximizing HSA contributions in your 30s provides a dedicated fund for future healthcare needs. Additionally, after age 65, you can withdraw HSA funds for any purpose without penalty, though non-medical withdrawals are taxed as ordinary income.

Starting Late: Strategies for Accelerated Retirement Savings

Starting retirement planning at 30 with no savings requires aggressive strategies to compensate for lost time. However, your 30s still provide sufficient runway for substantial wealth accumulation through disciplined saving and smart investing.

Maximizing Employer Benefits and Tax Advantages

Leveraging employer benefits accelerates your retirement savings journey. Beyond 401(k) matching, explore other benefits like profit-sharing plans, employee stock purchase plans (ESPPs), and pension plans if available. Additionally, understanding your total compensation package helps you make informed career decisions.

Tax-advantaged retirement accounts provide powerful benefits for Americans building wealth. Pre-tax contributions to Traditional 401(k)s and IRAs reduce your current tax bill while allowing investments to grow tax-deferred. For example, a single filer earning $60,000 who contributes $6,000 to a Traditional IRA reduces their taxable income to $54,000, saving approximately $1,320 in federal taxes (at 22% tax bracket).

Furthermore, tax credits like the Saver’s Credit benefit low-to-moderate-income Americans. This credit provides up to $1,000 ($2,000 for married couples) for retirement contributions, effectively reducing your tax bill while building retirement savings. Consequently, research all available tax incentives when planning your retirement strategy.

Increasing Your Income Through Side Hustles

Boosting your income accelerates retirement savings significantly. Side hustles, freelancing, or starting a small business provides additional funds specifically for retirement contributions. Moreover, side hustle strategies and side hustle stack approaches help you diversify income streams and build wealth faster.

Additionally, consider passive income opportunities like rental properties or passive income on Amazon. These ventures can generate ongoing revenue that flows directly into retirement accounts. For example, earning an extra $500 monthly from side income and investing it could add $200,000 to your retirement nest egg over 30 years.

Career advancement also boosts retirement contributions. Negotiating salary increases, pursuing promotions, or changing jobs for better compensation directly impacts retirement savings capacity. Furthermore, directing raises and bonuses straight into retirement accounts prevents lifestyle inflation while accelerating wealth building.

Implementing Aggressive Savings Strategies

Americans serious about catching up on retirement savings must adopt aggressive saving techniques. Start by identifying areas to cut expenses without sacrificing quality of life. For instance, saving money when selling your house and reducing credit card processing fees free up additional funds for retirement.

Consider aggressively saving money through challenges like no spend challenges that help identify unnecessary expenses. Additionally, implementing the savings plan formula provides a structured approach to building wealth systematically.

Furthermore, automating your savings ensures consistency. Set up automatic transfers from your checking account to retirement accounts immediately after each paycheck. This “pay yourself first” approach removes temptation while building wealth consistently. Moreover, gradually increase your savings rate annually by 1-2% to accelerate progress without feeling deprived.

Building Wealth Through Smart Investing

Investment knowledge is crucial when starting retirement planning at 30 with no savings. Understanding basic investing principles helps you make informed decisions and avoid costly mistakes that could derail your retirement goals.

Diversification and Asset Allocation Basics

Diversification protects your retirement portfolio from market volatility. Rather than putting all funds in one investment, spread money across various asset classes including stocks, bonds, and real estate. Additionally, Modern Portfolio Theory provides frameworks for optimizing diversification and risk management.

Asset allocation depends on your age, risk tolerance, and retirement timeline. A common rule suggests subtracting your age from 110 to determine your stock allocation percentage. For example, a 30-year-old might allocate 80% to stocks and 20% to bonds. Consequently, younger investors can tolerate more volatility because they have decades to recover from market downturns.

Target-date funds simplify asset allocation by automatically adjusting investments as you approach retirement. These funds start with higher stock allocations and gradually shift toward bonds and cash as the target retirement date nears. Therefore, they’re excellent options for hands-off investors seeking professional management.

Understanding Investment Fees and Their Impact

Investment fees significantly impact long-term retirement wealth. Even small fee differences compound dramatically over decades. For example, a 1% annual fee difference on a $100,000 investment over 30 years could cost you over $60,000 in lost returns.

Therefore, prioritize low-cost index funds and ETFs over actively managed funds. Index funds typically charge 0.03-0.20% annual fees compared to 0.5-2.0% for actively managed funds. Additionally, most actively managed funds fail to beat their benchmark indexes over long periods, making low-cost passive investing the superior choice for most retirement savers.

Furthermore, avoid investment products with high expense ratios, load fees, or excessive trading costs. These fees drain your retirement account without providing commensurate value. Consequently, research fund expenses carefully before investing and strongly prefer low-cost options from reputable providers like Vanguard, Fidelity, or Schwab.

Long-Term Growth Strategies

Successful retirement investing requires patience and discipline. Avoid the temptation to time the market or chase hot stock tips. Instead, adopt a long-term buy-and-hold strategy that capitalizes on compound growth. Additionally, dollar-cost averaging—investing consistent amounts regularly—smooths out market volatility and removes emotional decision-making.

Market downturns are inevitable and should be expected. However, they represent buying opportunities rather than panic-selling triggers. Americans who maintained their investment strategies during the 2008 financial crisis and 2020 pandemic crash saw their portfolios recover and reach new highs. Therefore, stay invested through market cycles and resist the urge to abandon your strategy during turbulent times.

Furthermore, regularly rebalance your portfolio to maintain target asset allocations. As investments grow at different rates, your asset allocation drifts from your target. Rebalancing annually or semi-annually ensures your portfolio maintains appropriate risk levels for your age and goals.

Maximizing Retirement Contributions on Limited Income

Starting retirement planning at 30 with no savings often means limited resources for contributions. However, even modest contributions grow substantially over time through compound interest. Moreover, creative strategies help maximize retirement savings despite income constraints.

Starting Small and Building Momentum

Don’t let perfect be the enemy of good. Contributing $50 or $100 monthly beats contributing nothing while you wait for ideal circumstances. Additionally, small contributions build the saving habit and create momentum. For instance, starting with $100 monthly and increasing contributions by just $25 annually could result in over $150,000 after 30 years at 7% returns.

Furthermore, direct windfalls like tax refunds, bonuses, or inheritances straight into retirement accounts. These lump-sum contributions accelerate wealth building without impacting your monthly budget. For example, investing a $2,000 tax refund annually for 30 years yields approximately $240,000 at 7% returns.

Additionally, gradually increase retirement contributions as your income grows. Commit to directing half of all raises toward retirement savings. This approach accelerates wealth building while still allowing lifestyle improvements. Consequently, you’ll barely notice the increased savings rate while dramatically boosting your retirement nest egg.

Using Catch-Up Opportunities Strategically

While traditional catch-up contributions don’t start until age 50, you can still “catch up” in your 30s by maximizing contributions whenever possible. Additionally, if you experience years with higher income, consider maxing out all available retirement accounts—401(k), IRA, and HSA—during those periods.

Furthermore, if your employer allows after-tax 401(k) contributions beyond the standard limit, consider mega backdoor Roth conversions. This strategy allows high earners to contribute significantly more to retirement accounts while enjoying Roth tax treatment on future growth. However, this complex strategy requires careful planning and professional guidance.

Moreover, if you’re self-employed or have side business income, establish a SEP-IRA or solo 401(k). These accounts offer substantially higher contribution limits than traditional IRAs, allowing you to sock away more money for retirement. For 2025, SEP-IRA contributions can reach up to 25% of compensation or $69,000, whichever is less.

Balancing Multiple Financial Goals

Americans in their 30s often juggle competing financial priorities. Student loans, mortgages, emergency funds, and retirement savings all demand attention. However, you can’t afford to completely ignore retirement while addressing other goals.

Adopt a balanced approach that addresses critical needs while building retirement savings. First, establish a minimal emergency fund of $1,000-$2,000 for unexpected expenses. This prevents you from raiding retirement accounts during financial emergencies. Additionally, understanding emergency fund best practices helps you build adequate financial cushions.

Subsequently, contribute enough to your 401(k) to capture the full employer match—this is free money you can’t afford to leave on the table. Then, focus on high-interest debt elimination while maintaining minimum payments on other obligations. Finally, increase retirement contributions progressively as debt decreases and income grows.

Furthermore, recognize that some debt is acceptable while building retirement wealth. Low-interest mortgages and federal student loans shouldn’t prevent retirement saving entirely. Instead, make strategic minimum payments while directing excess funds toward retirement accounts. The key is finding the right balance for your specific situation.

Why Starting Retirement Planning at 30 Matters

Understanding the importance of early retirement planning motivates consistent action and discipline. Americans who start saving in their 30s position themselves for comfortable retirements, while those who delay face increasing challenges. Moreover, time is the most powerful factor in wealth accumulation through compound interest.

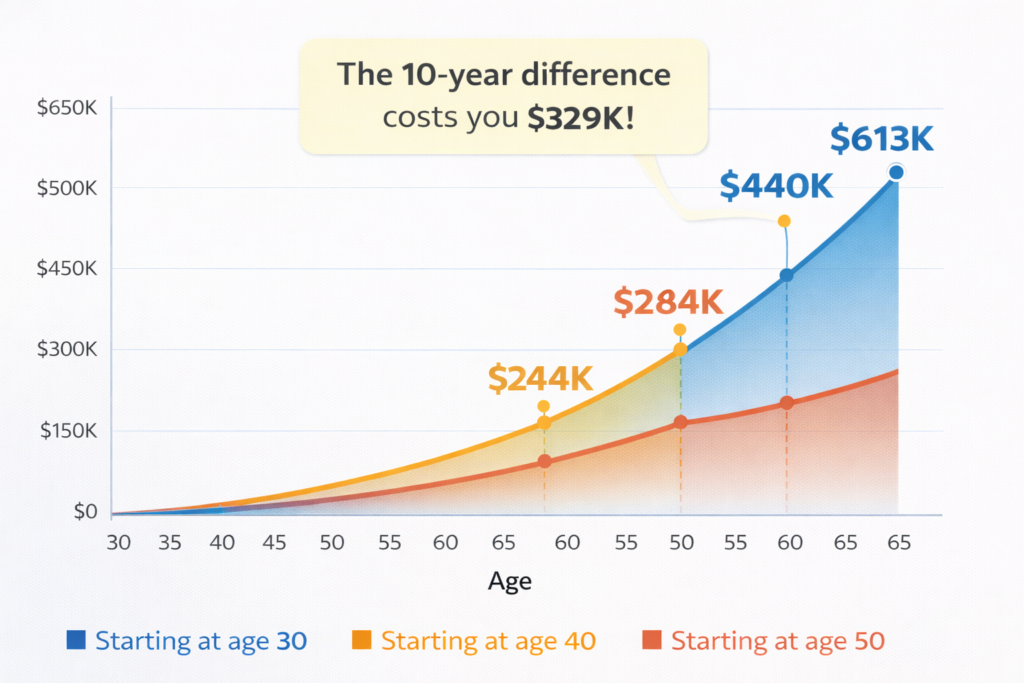

The Power of Compound Interest Over Three Decades

Compound interest is often called the eighth wonder of the world for good reason. It transforms modest contributions into substantial wealth over time. Consider this: investing $500 monthly starting at age 30 with 7% annual returns yields approximately $613,000 by age 65. However, waiting until age 40 to start reduces that to approximately $284,000—less than half despite only a 10-year delay.

Furthermore, compounding accelerates dramatically over time. In the early years, growth comes primarily from contributions. However, eventually investment returns dwarf new contributions. For example, in year 30 of the scenario above, annual investment growth exceeds $40,000 while annual contributions total just $6,000. Therefore, starting early gives compounding more time to work its magic.

Additionally, consistent long-term investing smooths out market volatility. While short-term market fluctuations are inevitable, three decades of investing captures multiple market cycles and delivers strong average returns. Consequently, time in the market beats timing the market, making an early start crucial for retirement success.

Avoiding Financial Stress in Later Life

Americans who neglect retirement planning in their 30s face increased financial pressure later. By your 40s and 50s, competing demands intensify—college expenses, aging parent care, and increased healthcare costs. Moreover, your earning potential may plateau or decline. Therefore, establishing retirement savings habits in your 30s prevents scrambling to catch up when financial flexibility decreases.

Furthermore, starting retirement planning early provides peace of mind and reduces financial anxiety. Knowing you’re building a nest egg alleviates worry about your financial future. Additionally, adequate retirement savings provides flexibility for career changes, entrepreneurship, or early retirement if desired. Consequently, early planning creates options rather than limiting them.

Moreover, Social Security likely won’t provide sufficient retirement income alone. The average Social Security retirement benefit in 2025 is approximately $1,920 monthly—barely enough to cover basic expenses for most Americans. Therefore, personal retirement savings become essential for maintaining your desired lifestyle in retirement.

Achieving Financial Independence and Retirement Options

Starting retirement planning at 30 with no savings ultimately leads to financial independence—the ability to live on your terms without financial constraints. Moreover, aggressive early saving opens possibilities like early retirement, semi-retirement, or pursuing passion projects without financial worry.

The FIRE movement (Financial Independence, Retire Early) demonstrates how disciplined saving and investing in your 30s enables retirement in your 40s or 50s. While extreme frugality isn’t necessary, the underlying principles apply: maximize savings rates, invest wisely, and let compound interest work for decades. Consequently, you gain control over your time and life direction rather than being chained to financial necessity.

Additionally, adequate retirement savings allows you to pursue meaningful work rather than just financially necessary employment. You can take career risks, start businesses, or shift to lower-paying but more fulfilling careers without jeopardizing your retirement security. Furthermore, financial independence provides resilience against job loss, economic downturns, or health challenges that might otherwise devastate your finances.

Step-by-Step Guide to Starting Your Retirement Plan

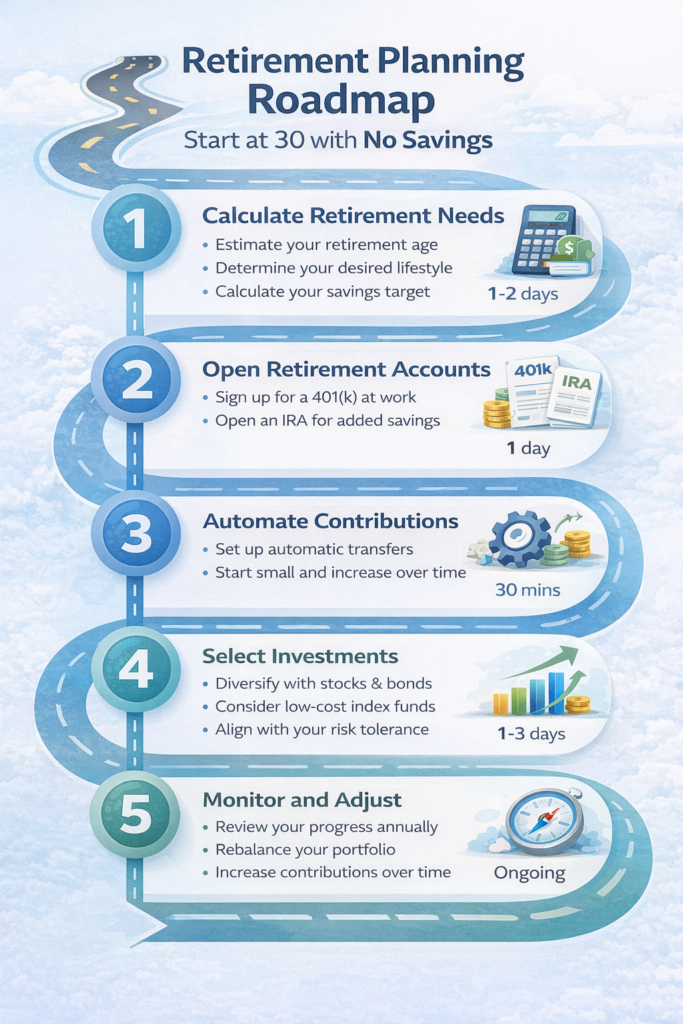

Creating and implementing a retirement plan requires systematic action. Following these structured steps helps Americans in their 30s build solid retirement foundations despite starting with no savings.

Step 1: Calculate Your Retirement Needs

Begin by estimating your retirement expenses. Financial planners often recommend replacing 70-80% of your pre-retirement income. However, your specific needs depend on planned lifestyle, healthcare costs, and desired activities. Additionally, factor in inflation—money’s purchasing power decreases approximately 3% annually.

Use retirement calculators to estimate how much you’ll need. For example, retirement planning calculators help determine whether your savings trajectory meets your goals. Generally, Americans need approximately 25 times their annual retirement expenses saved to sustain a 4% withdrawal rate indefinitely. Therefore, someone needing $50,000 annually would need $1.25 million saved.

Furthermore, consider how much money you need to retire in the USA based on location and lifestyle preferences. Cost of living varies dramatically across the country, affecting retirement savings requirements. Consequently, factor in where you plan to retire when calculating your target nest egg.

Step 2: Open Appropriate Retirement Accounts

After assessing needs, establish the right retirement accounts. Start with employer-sponsored plans like 401(k)s if available. Complete enrollment paperwork, select investments, and designate contribution percentages. Additionally, set contributions to at least capture the full employer match immediately.

Subsequently, open an IRA—either Traditional or Roth based on your tax situation and income level. Most major brokerages offer free IRA accounts with no minimum balances. Choose reputable providers with low fees and strong customer service. Furthermore, if eligible, establish an HSA for triple tax advantages on healthcare savings.

Moreover, consolidate old retirement accounts from previous employers. Rolling 401(k)s from former jobs into an IRA simplifies management and often reduces fees. However, evaluate each situation carefully—some employer plans offer unique benefits worth preserving. Consequently, research thoroughly before making rollover decisions.

Step 3: Create and Automate Your Contribution Strategy

Automation ensures consistent retirement contributions without relying on willpower. Set up automatic paycheck deductions for employer retirement plans. Additionally, schedule automatic transfers from checking accounts to IRAs immediately after payday. This “pay yourself first” approach treats retirement savings as a non-negotiable expense.

Start with whatever amount fits your budget, then increase progressively. Many 401(k) plans offer automatic escalation features that increase contribution percentages annually. For example, starting at 5% and increasing by 1% yearly reaches 15% after a decade—a substantial savings rate achieved gradually. Therefore, leverage automation to steadily increase retirement contributions without feeling deprived.

Furthermore, direct all raises and bonuses toward retirement savings for several years. This strategy accelerates wealth building while maintaining your current lifestyle. Additionally, when debt payments end, immediately redirect those funds into retirement accounts rather than spending increases.

Step 4: Select Appropriate Investments

Investment selection determines your retirement portfolio’s growth trajectory. For most Americans in their 30s, target-date funds offer simple, effective solutions. These funds automatically adjust asset allocation from aggressive (stock-heavy) to conservative (bond-heavy) as retirement approaches. Consequently, they remove the guesswork from investment management.

Alternatively, build your own portfolio using low-cost index funds. A simple three-fund portfolio—total stock market index, total international stock index, and total bond market index—provides adequate diversification with minimal fees. Additionally, rebalance annually to maintain target allocations as different assets grow at varying rates.

Moreover, educate yourself on financial literacy basics to make informed investment decisions. Understanding fundamental concepts like risk tolerance, diversification, and compound interest helps you navigate investment choices confidently. Furthermore, consider working with a fee-only financial advisor for personalized guidance.

Step 5: Monitor Progress and Adjust Regularly

Retirement planning requires regular review and adjustment. Check account balances quarterly to track progress toward goals. However, avoid obsessive monitoring that might trigger emotional reactions to short-term market fluctuations. Additionally, review and rebalance your portfolio annually to maintain appropriate asset allocations.

Furthermore, reassess retirement goals every few years as life circumstances change. Marriage, children, career changes, and health issues all impact retirement planning. Consequently, adjust savings rates, investment strategies, and target retirement dates as needed to reflect current realities and future aspirations.

Moreover, take advantage of financial planning resources and professional guidance when needed. Complex situations like business ownership, significant windfalls, or major life transitions warrant professional financial planning assistance. Additionally, asking the right questions to financial advisors ensures you receive valuable, unbiased advice.

Protecting Your Retirement Savings

Building retirement wealth is only half the equation—protecting those assets is equally important. Americans face various threats to retirement savings, from market volatility to healthcare costs. Therefore, implementing protective strategies safeguards your financial future.

Insurance as Part of Retirement Planning

Adequate insurance coverage protects retirement assets from catastrophic losses. Health insurance prevents medical bills from decimating retirement savings. Moreover, understanding why insurance is important in financial planning helps you prioritize appropriate coverage.

Disability insurance replaces income if you become unable to work, ensuring retirement contributions continue despite health setbacks. Furthermore, life insurance protects dependents and retirement plans if you die prematurely. While term life insurance costs far less than permanent policies, it provides adequate protection for most Americans in their 30s.

Additionally, long-term care insurance warrants consideration, especially for those with family histories of chronic illness or dementia. Long-term care costs can destroy retirement savings rapidly. Therefore, purchasing coverage in your 50s or 60s—while premiums remain affordable and health issues minimal—protects retirement assets from nursing home or extended care expenses.

Avoiding Common Retirement Savings Mistakes

Americans often make predictable mistakes that derail retirement planning. First, avoid withdrawing retirement funds for non-emergencies. Early withdrawals trigger taxes and penalties while permanently reducing future wealth through lost compound growth. Additionally, loans against 401(k) accounts should be last resorts, not convenient funding sources for discretionary purchases.

Furthermore, resist the temptation to chase investment fads or hot stock tips. These speculative investments rarely deliver promised returns and often result in significant losses. Instead, maintain disciplined, diversified investment strategies despite market noise and media hype. Moreover, understand why personal finance depends on behavior—emotional decisions typically hurt long-term wealth building.

Additionally, don’t neglect beneficiary designations on retirement accounts. These designations supersede wills, making them critical estate planning documents. Review and update beneficiaries after major life events like marriages, divorces, births, or deaths. Consequently, your retirement assets transfer according to your wishes rather than default legal provisions.

Building Multiple Income Streams for Retirement

Diversifying retirement income sources reduces risk and increases financial security. While traditional retirement accounts form the foundation, consider additional income streams. Rental properties generate passive income through real estate appreciation and monthly rent. Moreover, dividend-paying stocks provide regular income without selling assets.

Furthermore, part-time work or consulting in retirement supplements savings while keeping you engaged and active. Many retirees discover fulfilling second careers that generate income without the stress of full-time employment. Additionally, businesses built in your 30s and 40s can provide ongoing income or valuable sale proceeds boosting retirement security.

Social Security provides baseline income, but maximizing benefits requires strategic planning. Delaying claims until age 70 increases monthly benefits by approximately 8% annually after full retirement age. Therefore, if you can afford to wait, delaying Social Security claims substantially boosts lifetime income. However, claiming earlier makes sense for those with health issues or insufficient other retirement income.

FAQ

Q: Can I really start retirement planning at 30 with no savings and still retire comfortably?

Yes, absolutely. Starting retirement planning at 30 with no savings gives you 35+ years until traditional retirement age. With consistent contributions and reasonable investment returns, you can build substantial retirement wealth. For example, contributing $500 monthly from age 30 to 65 with 7% returns yields approximately $613,000. Additionally, increasing contributions as income grows accelerates wealth building significantly. The key is starting immediately and maintaining discipline throughout your career.

Q: How much should a 30-year-old with no savings contribute to retirement accounts?

Financial experts recommend saving 15% of gross income for retirement. However, if starting with no savings at 30, consider increasing to 20% if possible. Start with whatever you can afford—even 5% is better than nothing. Additionally, always contribute enough to capture full employer 401(k) matching. Furthermore, increase contributions by 1-2% annually or direct half of all raises toward retirement. This gradual approach reaches substantial savings rates without feeling overwhelming.

Q: What’s the biggest mistake people make when starting retirement planning late?

The biggest mistake is delaying further due to feeling overwhelmed or behind. Starting today, even with minimal contributions, beats waiting for perfect circumstances that may never arrive. Additionally, many people chase high-risk investments trying to “catch up” quickly, often losing money instead. Moreover, failing to capture employer 401(k) matching leaves free money on the table. Consequently, start immediately with small amounts, invest conservatively, and capture all employer matches to avoid these common pitfalls.

Q: Should I pay off debt or save for retirement first?

Balance both simultaneously. Contribute enough to capture full employer 401(k) matching immediately—this is non-negotiable. Then, focus on high-interest debt (credit cards, payday loans) while making minimum retirement contributions. Furthermore, once high-interest debt is eliminated, redirect those payments toward increased retirement savings. However, don’t delay retirement saving completely to pay off low-interest debt like mortgages or federal student loans. The opportunity cost of delayed retirement contributions often exceeds interest saved on low-rate debt.

Q: What if my employer doesn’t offer a 401(k) plan?

Open an IRA immediately—either Traditional or Roth based on your tax situation. For 2025, you can contribute up to $7,000 annually. Additionally, if self-employed, establish a SEP-IRA or solo 401(k) with much higher contribution limits. Furthermore, advocate for your employer to establish a retirement plan—many small businesses are unaware of simplified options like SIMPLE IRAs. Moreover, consider whether job change to an employer offering retirement benefits makes sense for your long-term financial health. Retirement benefits represent significant compensation components worth considering in career decisions.

Take Action Today: Your Retirement Future Starts Now

Starting retirement planning at 30 with no savings is challenging but completely achievable. Every day you delay costs you valuable compound growth that can never be recovered. Therefore, commit to taking action today—even small steps create momentum toward financial security.

Begin by opening a retirement account this week. If your employer offers a 401(k), complete enrollment immediately. Additionally, open an IRA if you haven’t already. Set up automatic contributions—start with just $100 monthly if that’s all you can afford. Furthermore, schedule an annual review to increase contributions and assess progress toward retirement goals.

Moreover, educate yourself continuously on personal finance topics. Read books, follow reputable financial blogs, and consider working with fee-only financial advisors for personalized guidance. Understanding financial principles empowers you to make informed decisions that accelerate wealth building. Additionally, surround yourself with financially savvy friends who support your retirement planning goals rather than encouraging unnecessary spending.

Remember, retirement planning is a marathon, not a sprint. Consistency matters far more than perfect timing or ideal circumstances. Americans who start saving in their 30s and maintain discipline throughout their careers retire comfortably regardless of starting balances. Therefore, focus on what you can control—savings rates, investment choices, and spending habits—rather than worrying about market volatility or economic uncertainty.

Your financial future depends on actions you take today. Starting retirement planning at 30 with no savings isn’t ideal, but it’s far from hopeless. With commitment, discipline, and smart strategies, you can build the retirement wealth necessary for financial independence and security. Begin your journey today—your future self will thank you for decades to come.

Karthick Raja, MBA, is a personal finance educator and HR professional with 10+ years of experience in Personal Finance ,taxation, payroll, and career development. He helps readers build wealth, manage money wisely, and grow professionally.