If you’re 40 and looking at your retirement savings with a sense of concern, you are not alone. The weight of that “late start” can feel substantial. However, in the world of financial planning, 40 is not an endpoint—it’s a strategic inflection point. You bring to the table resources, higher earning potential, and financial clarity that your 25-year-old self-likely didn’t have. This guide is your blueprint for leveraging those advantages. It will provide a clear path forward, grounded in the math of compound growth curves, the specific rules of the U.S. Regulatory Landscape, and a tailored Strategic Asset Allocation for a 20–25-year horizon. It is not too late to build a secure and dignified retirement.

The Core Mindset: Clarity Over Anxiety

The first step is to replace anxiety with a clear-eyed assessment. The conventional advice to “start early” exists for a reason, but dwelling on the past is counterproductive. Your focus must now be on maximization and efficiency. Every financial decision, from your monthly budget to your investment selections, must be evaluated through this lens. Your goal is to accelerate savings growth by combining higher contributions with smart, rules-based strategies designed for your timeline. This approach transforms the challenge into a manageable and empowering project.

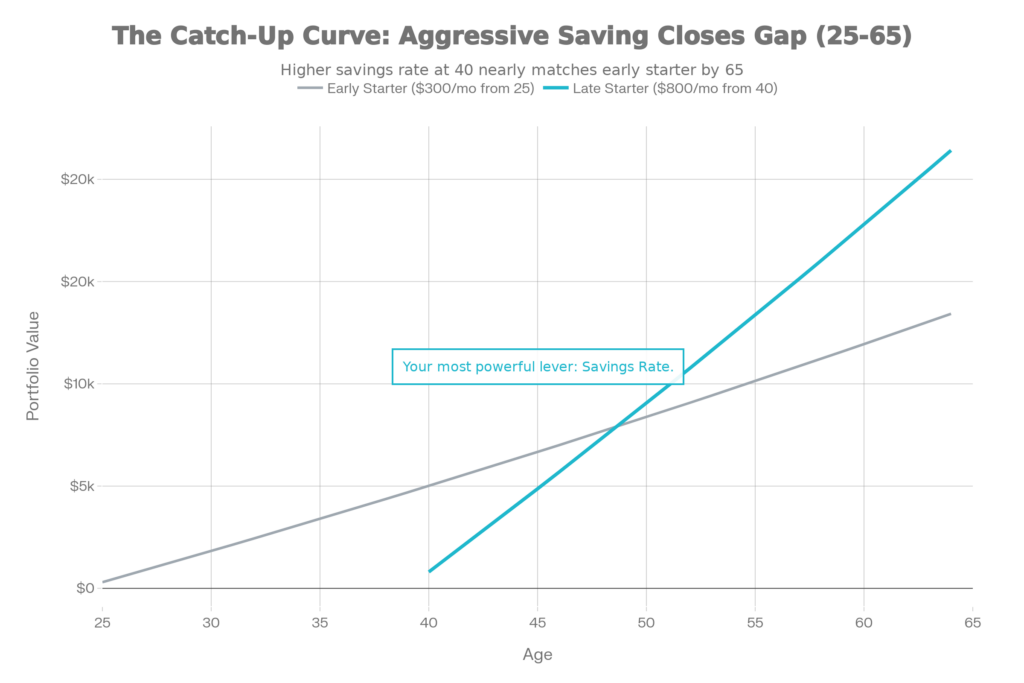

The “Math of 40”: Your Accelerated Trajectory

Understanding the numerical reality is empowering. While starting early has undeniable benefits due to compound interest, starting at 40 with discipline can yield powerful results. The key differentiator is your contribution rate.

The table below illustrates the potential outcomes by age 65, assuming a conservative average annual return of 6%. It highlights the dramatic impact of maximizing contributions, especially by utilizing catch-up contributions available to those 50 and older.

| Monthly Contribution | Total Contributions by 65 | Estimated Value at 65 (6% avg return) | Key Strategy Notes |

|---|---|---|---|

| $500 | $150,000 | ~$290,000 | A baseline start. Focus on consistency and avoiding fees. |

| $1,250 | $375,000 | ~$725,000 | Nears the 2025 IRA max ($7,000). A strong, disciplined target. |

| $1,875 | $562,500 | ~$1.09 million | Reaches the 2025 401(k) employee max ($23,000). A highly aggressive pace. |

| $2,500+ | $750,000+ | ~$1.45 million+ | Incorporates catch-up contributions, taxable investing, or HSA savings. |

Analysis: The jump from $500 to $1,875 monthly is a 275% increase in contributions, but it leads to a 276% increase in the ending portfolio value. This near 1:1 relationship in this timeframe shows that your savings rate is your most powerful lever. The growth is driven more by your substantial new capital than by decades of compounding interest. This math validates that aggressive saving starting now can still build a formidable nest egg.

The U.S. Regulatory Landscape: Rules for the Mid-Life Saver

Your strategy must be built within the framework of U.S. tax and retirement account laws. Knowing these rules allows you to squeeze every possible dollar into tax-advantaged accounts.

- 2025 Contribution Limits: For 2025, you can contribute up to $23,000 to a 401(k), 403(b), or similar employer plan. You can contribute up to $7,000 to an IRA (Traditional or Roth). These are the boundaries of your primary savings battlefield.

- The Catch-Up Provision: Once you turn 50, the IRS allows you to contribute extra “catch-up” amounts. This is a non-negotiable part of your plan. In 2025, the 401(k) catch-up is $7,500 (bringing the total limit to $30,500), and the IRA catch-up is $1,000 (bringing the total to $8,000).

- The Critical Importance of Vesting: If your employer offers a matching contribution, understanding your plan’s vesting schedule is urgent. “Vesting” means earning the right to keep those employer-matched funds if you leave the company. At this stage in your career, you must prioritize staying at a job long enough to become fully vested; leaving early could mean forfeiting what is essentially free money crucial to your catch-up plan.

- Social Security Credits: Your future Social Security benefits are calculated based on your 35 highest-earning years. Starting at 40, you have 25+ years until full retirement age, meaning you have ample time to replace low- or zero-earning years from your youth with higher-earning ones, positively boosting your benefit calculation.

Strategic Asset Allocation for a 20–25 Year Horizon

With a shorter timeline, your investment strategy must balance growth potential with prudent risk management. The old “100 minus your age” rule (suggesting a 60% stock allocation at 40) is being questioned by many today for being too conservative for longer lifespans. Your allocation requires more nuance.

Re-Thinking “100 Minus Your Age”

While this rule provides a simple starting point, a static formula may not suit your need for growth. A 60/40 stock/bond split might be a foundation, but given your need for portfolio growth, a moderately higher equity allocation (e.g., 70-75% stocks) could be appropriate if you have the risk tolerance. The key is that this allocation isn’t static; it should glide toward conservatism as you approach retirement.

Building a Resilient Core Portfolio

Your portfolio should be built on low-cost, diversified index funds or ETFs. This ensures you capture broad market growth without the drag of high fees. Diversification across U.S. stocks, international stocks, and bonds is your primary defense against volatility. Given your timeline, your focus should be on consistently adding shares—a process that buys more when prices are low and fewer when they are high, smoothing your path over time.

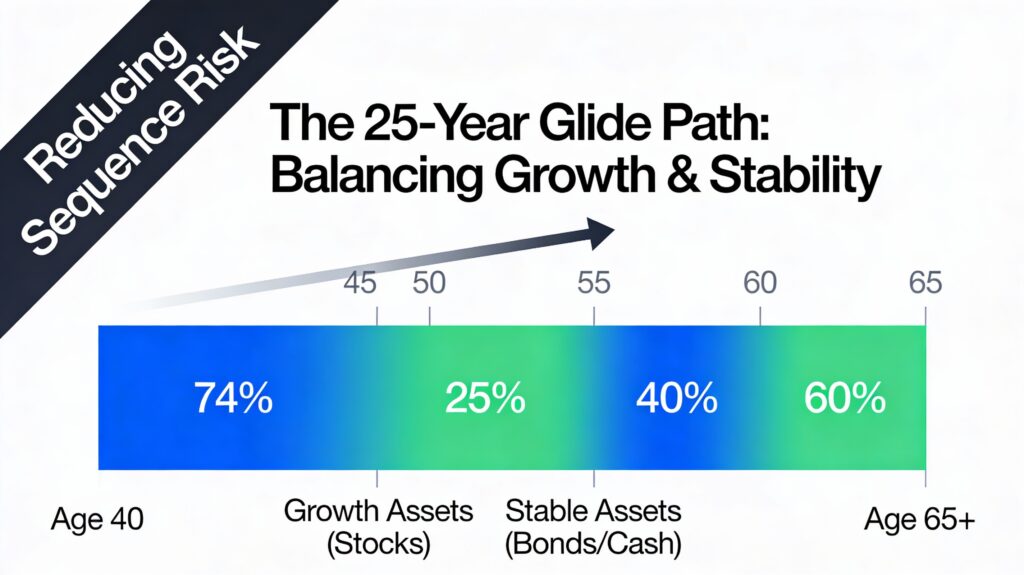

The Sequence of Returns Risk: Your New Focus

As you approach retirement (in your late 50s and early 60s), a new risk becomes paramount: the sequence of returns risk. This is the danger that a major market downturn in the years just before or after you retire could permanently deplete your portfolio. Your asset allocation strategy must gradually evolve to mitigate this. This often means building a “retirement bridge” of 2-5 years of living expenses in cash or short-term bonds as you transition into retirement, allowing your long-term investments time to recover from any downturn.

FAQ

1. Is it really possible to save enough starting this late?

Yes, absolutely. It requires a higher savings rate than someone who started at 25, but it is mathematically feasible. As the table in “The Math of 40” shows, consistent, aggressive saving can still build a portfolio worth $1 million or more. Your success will be defined by your savings discipline, not just market returns.

2. Should I prioritize a Traditional 401(k)/IRA or a Roth?

This is a critical tax diversification question. A Traditional account gives you a tax deduction now (lowering your current tax bill), while a Roth offers tax-free growth and withdrawals later. A strong strategy for many mid-life starters is to split contributions: fund a Traditional 401(k) up to the employer match, then direct additional savings to a Roth IRA (if income-eligible) or a Roth 401(k). This gives you flexible income sources in retirement to manage your tax bracket.

3. What is the “4% rule,” and does it still work?

The 4% rule is a traditional guideline suggesting you can withdraw 4% of your initial retirement portfolio in the first year, adjusted for inflation each year after, with a high probability of your money lasting 30 years. Its relevance is actively debated due to current economic conditions. While a useful starting point for planning, you should treat it as a flexible guideline, not a guarantee. In practice, you may need to be prepared for a lower initial withdrawal rate or to adjust spending based on market performance.

4. I have multiple old 401(k)s. What should I do with them?

Consolidate them. Rolling old employer plans into a single Rollover IRA or your current employer’s 401(k) simplifies management, reduces fees, and provides a clear view of your total assets. This consolidation is a crucial administrative step in taking control of your retirement strategy.

5. What is a “Roth conversion ladder,” and should I consider it?

A Roth conversion ladder is an advanced strategy where you systematically convert portions of a Traditional IRA to a Roth IRA over several years, paying taxes on the converted amount at the time of conversion. The funds become tax-free after a five-year waiting period. For a mid-life starter, this can be a powerful tool in early retirement to access funds before age 59½ without penalty and to manage long-term tax liability. It requires careful multi-year planning.

Disclaimer: This article is for educational and informational purposes only and does not constitute personalized financial advice. Your financial situation is unique. You should consult with a qualified financial advisor, before making any financial decisions.