You wake up on your 60th birthday and the realization hits: you have little to nothing saved for retirement. Your hands shake as you check your bank balance. The panic sets in. You’re not alone—according to recent AARP research, one in five Americans over 50 have no retirement savings whatsoever, and 61% worry they won’t have enough money to support themselves in their later years.

But here’s what the financial industry doesn’t want you to know: it’s not too late. While you won’t build a seven-figure nest egg at this stage, you can absolutely create a secure, dignified retirement with strategic action starting today.

This comprehensive guide will show you exactly What to Do If You’re 60 With No Retirement Savings, step by step. No judgment. No false promises. Just proven strategies that work.In this article we will seen What to Do If You’re 60 With No Retirement Savings

Understanding Your Current Reality

The Truth About Starting Late

Let’s be honest: starting retirement savings at 60 is challenging. You’ve missed decades of compound interest growth that younger savers enjoy. But dwelling on past mistakes won’t change your future—taking action will.

The average Social Security payment for retired workers is $2,006.69 per month. For many Americans approaching retirement age with no savings, this becomes their primary income source. The question isn’t whether you can survive—it’s how you can thrive with strategic planning.

Why You’re in This Situation (And Why It Doesn’t Matter)

Whether you experienced:

- Job losses during economic downturns

- Medical emergencies that drained savings

- Divorce or family financial crises

- Supporting children or aging parents

- Simply living paycheck to paycheck

The reasons don’t matter anymore. What matters is what you do next.

Related: Why is personal finance dependent upon your behavior

Immediate Action Steps: Your First 30 Days

Step 1: Stop the Bleeding – Create a Zero-Based Budget

Your very first priority is building a zero-based budget for the next 60 days. Track every single expense to confirm your real baseline spending. This isn’t punishment—it’s power. You can’t change what you don’t measure.

Action Items:

- Download a budgeting app or use a simple spreadsheet

- Record every expense for 60 days

- Categorize spending into needs vs. wants

- Identify immediate cuts you can make

Learn more: The Savings Plan Formula

Step 2: Assess Your Complete Financial Picture

Create a comprehensive financial inventory:

Assets:

- Home equity value

- Vehicle value

- Any savings accounts

- Investment accounts (however small)

- Life insurance cash value

- Personal property with resale value

Liabilities:

- Mortgage balance

- Credit card debt

- Auto loans

- Personal loans

- Medical debt

Income Sources:

- Current employment income

- Potential Social Security benefits (check ssa.gov)

- Pension benefits (if any)

- Spousal income

Step 3: Make the Hard Decision About Debt

If you’re carrying high-interest debt (20% APR or higher), prioritize paying it down immediately while simultaneously starting to save. For lower APR debt (3-5%), continue repaying while focusing more aggressively on retirement contributions.

Credit card interest is retirement savings in reverse. Every dollar going to interest payments is a dollar that could be working for your future.

Additional resource: How to fix credit after bankruptcy

Maximize Your Income: The Foundation of Recovery

The Brutal Truth About Your Current Job

If you’re working 25 hours a week as a cashier or in a similarly low-paying position, you need to face reality: that job won’t get you where you need to be. Financial expert Dave Ramsey puts it bluntly—you need a better job, period.

Immediate income boosting strategies:

- Negotiate Your Current Position

- Ask for additional hours

- Request a raise based on performance

- Take on additional responsibilities

- Explore Higher-Paying Fields

- Administrative roles (average $40,000-$55,000)

- Customer service management ($45,000-$65,000)

- Healthcare support roles ($35,000-$50,000)

- Government positions with benefits

- Leverage Life Experience

- Consulting in your previous career field

- Part-time specialized work

- Skills-based contracting

Building Additional Income Streams

The gig economy offers unprecedented opportunities for older workers:

Viable Options:

- Freelance consulting in your expertise area

- Online tutoring or teaching

- Virtual assistant services

- Part-time remote customer service

- Specialized skilled trades

- Pet sitting or house sitting services

Visit: Side Hustle Stack Guide

Important: Use American Job Centers

American Job Centers provide free resources including:

- Job matching services

- Skills training programs

- Resume assistance

- Interview preparation

- Connections to local employers

Find your nearest center at CareerOneStop.org

Strategic Retirement Savings at 60+

Maximize Catch-Up Contributions

The IRS provides special catch-up provisions for people 50 and older. Here’s what you can contribute in 2025:

401(k) Plans:

- Standard contribution: $23,500

- Catch-up contribution: $7,500

- Total possible: $31,000 annually

IRA (Traditional or Roth):

- Standard contribution: $7,000

- Catch-up contribution: $1,000

- Total possible: $8,000 annually

For married couples: If both spouses max out contributions, that’s $78,000 annually in tax-advantaged retirement savings.

The Power of Employer Matching

If your employer offers matching contributions, prioritize this above all else. An employer match is literally free money. Even a 4% match on a $50,000 salary adds $2,000 annually to your retirement fund.

Example Scenario: Let’s say you’re 60 and can contribute $26,000 to your 401(k) with a 4% employer match. Over 10 years with a conservative 7% return, you could accumulate approximately $360,000.

Related: How to set up a 401k for your small business

Investment Strategy for Late Starters

At 60, you don’t have time for ultra-conservative investments, but you also can’t afford major losses. A balanced approach works best:

Recommended allocation:

- 60% stock market index funds (growth potential)

- 30% bonds (stability)

- 10% cash or cash equivalents (emergency access)

Work with a certified financial planner to create a customized strategy. Organizations like the National Association of Personal Financial Advisors can connect you with fee-only advisors who work in your best interest.

Mastering Social Security Strategy

The Delayed Retirement Credit Advantage

This is perhaps your most powerful tool. For every year you delay claiming Social Security past your full retirement age (up to age 70), your monthly benefit increases by approximately 8%.

Real Numbers:

- Claiming at 62: Reduced benefit (possibly $1,500/month)

- Claiming at 67 (full retirement age): Full benefit ($2,400/month)

- Claiming at 70: Maximum benefit ($3,000/month)

That’s an extra $18,000 per year for life by waiting from 62 to 70. Over a 20-year retirement, that’s $360,000 in additional income.

Creating a Social Security Claiming Strategy

If you’re single: Delay as long as financially possible, ideally to age 70. The 8% annual increase is better than almost any guaranteed investment.

If you’re married: Coordinate claiming strategies with your spouse. Often, the higher earner should delay while the lower earner claims earlier. This maximizes survivor benefits.

If you’re divorced: You may be eligible for benefits based on your ex-spouse’s work record if the marriage lasted 10+ years. This doesn’t reduce their benefits.

Check your estimated benefits: Social Security Administration

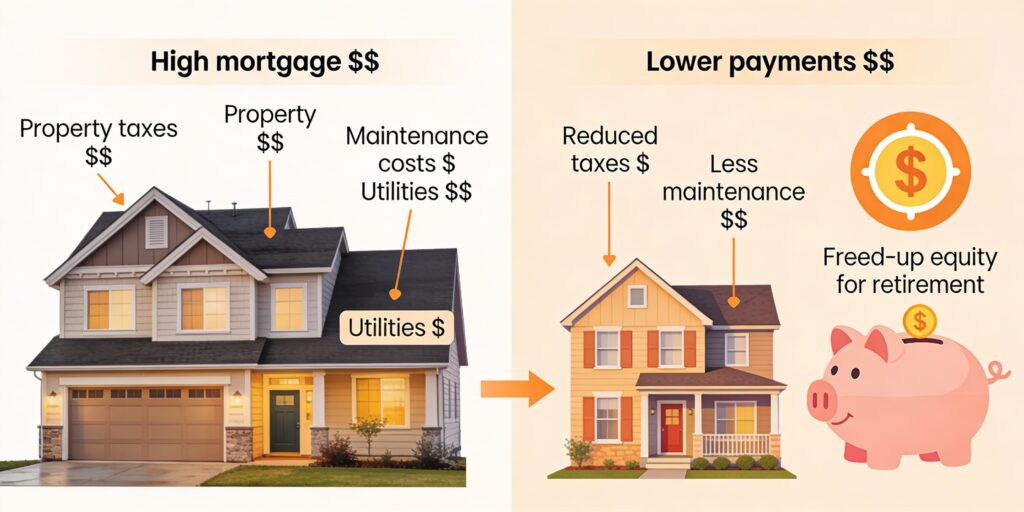

Housing: Your Biggest Asset and Liability

Should You Downsize?

If you own a home with substantial equity, downsizing could be transformative. Consider this scenario:

Before:

- Home value: $400,000

- Mortgage remaining: $150,000

- Equity: $250,000

After downsizing:

- Sell current home, net $250,000 equity

- Purchase smaller home for $180,000 cash

- Remaining funds: $70,000 for retirement savings

- Plus: Lower property taxes, maintenance, utilities, insurance

Alternative Housing Strategies

House hacking:

- Rent out a room or basement apartment

- Airbnb a spare room

- Take in a boarder

Relocation:

- Move to lower cost-of-living area

- Consider states with no income tax

- Research areas with lower property taxes

Reverse mortgages (proceed cautiously): Only consider as a last resort after consulting with a HUD-approved counselor. These can provide income but significantly reduce estate value.

More on real estate: How to save money when selling your house

Cutting Costs Without Sacrificing Quality of Life

The Big Three Expense Categories

Housing (aim for 25% of income)

- Refinance mortgage if rates are favorable

- Appeal property tax assessments

- Implement energy efficiency improvements

- Audit homeowner’s insurance annually

Transportation (aim for 10-15% of income)

- Consider one-car household

- Use public transportation

- Purchase reliable used vehicles instead of new

- Eliminate car payments entirely

Learn more: Saving on transportation

Food (aim for 10-15% of income)

- Meal planning prevents waste

- Buy generic brands

- Cook in batches

- Limit restaurant meals

Guide: Save big while you shop

Healthcare Cost Management

Before Medicare (under 65):

- Explore marketplace insurance subsidies

- Consider health sharing ministries

- Research state high-risk pools

- Look into COBRA alternatives

Medicare Planning (65+):

- Understand Parts A, B, C, and D

- Compare Medigap policies

- Review Part D plans annually

- Consider Medicare Advantage options

The transition to Medicare at 65 can save $500-800 monthly in health insurance costs—a massive boost to your budget.

The Subscription Audit

Most Americans waste $200-400 monthly on forgotten subscriptions. Review every recurring charge:

- Streaming services (keep only 1-2)

- Gym memberships (use free alternatives)

- Magazine subscriptions

- Software you don’t use

- Premium service tiers you don’t need

Government Assistance and Benefits

Programs You May Qualify For

Housing Assistance:

- Section 8 Housing Choice Voucher Program

- Public housing

- Low-Income Home Energy Assistance Program (LIHEAP)

Food Assistance:

- Supplemental Nutrition Assistance Program (SNAP)

- Local food banks

Employment Support:

- Senior Community Service Employment Program (SCSEP)

- Provides paid training and job placement

- Available through local Area Agencies on Aging

Healthcare:

- Medicaid (if income qualifies)

- Medicare Savings Programs

- Prescription drug assistance programs

Find benefits: Benefits.gov

There’s no shame in using programs you’ve paid into through decades of taxes. These exist precisely for situations like yours.

The Psychology of Late-Stage Retirement Planning

Overcoming Shame and Fear

Financial shame is a real barrier that prevents people from taking action. Research shows that money shame triggers the same brain responses as physical pain.

Reframe your thinking:

- You’re not “behind”—you’re starting now

- Every action improves your situation

- Millions face similar challenges

- Seeking help is strength, not weakness

Building Financial Resilience

Mental strategies that work:

- Focus on progress, not perfection

- Celebrate small wins weekly

- Find an accountability partner

- Join online communities of late-start savers

- Practice gratitude for what you have

Resource: 11 Financial planning tips from successful women

The Danger of Comparison

Stop comparing yourself to people with million-dollar nest eggs. Their journey isn’t yours. Focus exclusively on maximizing your own situation with the time and resources you have.

Creating Your Personalized 10-Year Plan

Year 1-2: Foundation Phase

Goals:

- Eliminate high-interest debt

- Max out employer 401(k) match

- Build $5,000 emergency fund

- Increase income by 20-30%

- Create sustainable budget

Year 3-5: Acceleration Phase

Goals:

- Max out catch-up contributions

- Build emergency fund to 6 months expenses

- Explore housing downsizing

- Establish secondary income source

- Achieve 30-40% savings rate

Year 6-10: Optimization Phase

Goals:

- Continue maxing retirement contributions

- Fine-tune Social Security claiming strategy

- Reduce fixed expenses by 20%

- Build $150,000+ retirement savings

- Develop part-time retirement work plan

Part-Time Work in Retirement

The New Retirement Reality

The old model of full retirement at 65 is dead. Most Americans now plan to work at least part-time in retirement, and this isn’t necessarily negative.

Benefits of working longer:

- Delays need to tap retirement savings

- Maximizes Social Security benefits

- Maintains social connections

- Provides sense of purpose

- Keeps mind sharp

Best Part-Time Retirement Jobs

Flexible, age-friendly options:

- Tax preparation (seasonal, good pay)

- Bookkeeping for small businesses

- Consulting in your expertise area

- Tutoring or teaching online

- Part-time retail in specialty stores

- Tour guide at museums/attractions

- Notary public services

- Grant writing for nonprofits

Target earnings: Even $15,000-20,000 annually from part-time work significantly extends retirement savings.

Related: 10 easy steps to start a hustle

Working With Financial Professionals

When to Seek Professional Help

You should consult professionals if:

- You have complex tax situations

- You’re considering selling your home

- You need to navigate Social Security strategy

- You have pension decisions to make

- You’re unsure about investment allocation

Finding the Right Advisor

Red flags to avoid:

- Commission-based advisors (conflicts of interest)

- Anyone promising guaranteed returns

- High-pressure sales tactics

- Advisors who won’t provide references

Look for:

- Certified Financial Planner (CFP) designation

- Fee-only compensation structure

- Fiduciary duty (legally required to act in your interest)

- Experience with clients in similar situations

- Clear, written fee structure

Organizations to check: CFP Board, National Association of Personal Financial Advisors

More guidance: Top 10 questions to ask your financial advisor

Real Success Stories

Case Study: Margaret and Her Husband

Margaret, 60, and her husband, 63, faced retirement with minimal savings. Here’s what they did:

Situation:

- Small existing retirement fund

- Still paying mortgage

- Margaret’s job offered no retirement benefits

Actions taken:

- Maxed out husband’s 401(k) with catch-up ($31,000/year)

- Both opened and maxed Roth IRAs ($16,000 combined)

- Downsized home, eliminating mortgage

- Margaret found higher-paying position

- Planned to delay Social Security until 70

Result: Projected $250,000+ in retirement savings by age 70, plus maximized Social Security benefits and debt-free living.

Common Mistakes to Avoid

Critical Errors That Derail Progress

- Taking Social Security Too Early

- Reduces lifetime benefits by 20-30%

- Impossible to reverse once started

- Ignoring Healthcare Costs

- The average couple needs $315,000 for healthcare in retirement

- Plan specifically for medical expenses

- Continuing to Support Adult Children

- You cannot borrow for retirement

- Your children can borrow for education

- Investing Too Conservatively

- At 60, you still need growth

- 100% bonds won’t build adequate savings

- Not Having a Written Plan

- Goals without plans are wishes

- Write it down, review monthly

Your Emergency Fund Strategy

Why It’s Non-Negotiable

Even in catch-up mode, you must build emergency savings. One unexpected expense can derail years of progress.

Target amounts:

- Start: $1,000 starter fund (month 1)

- Short-term: 3 months expenses (year 1)

- Long-term: 6 months expenses (years 2-3)

Where to keep it:

- High-yield savings account (4-5% APY)

- Money market account

- Treasury bills (for larger amounts)

Never in:

- Regular checking (too accessible)

- Investment accounts (market risk)

- Under the mattress (inflation risk)

Guide: What are three questions to ask yourself before spending your emergency fund

Insurance Protection in Your 60s

Essential Coverage

Health Insurance:

- Bridge coverage until Medicare (65)

- Understand all Medicare parts

- Consider long-term care insurance

Life Insurance:

- Term life if others depend on your income

- Enough to cover debts and final expenses

- Review beneficiaries annually

Disability Insurance:

- Critical if still working

- Protects your earning ability

- Especially important for self-employed

Property Insurance:

- Adequate homeowner’s coverage

- Umbrella policy if you have assets

- Review annually for adequate limits

Learn more: Why is insurance an important part of a financial plan

The Tax-Efficiency Factor

Strategic Tax Planning

Pre-tax vs. Roth Contributions:

- Traditional 401(k)/IRA: Tax deduction now, pay taxes in retirement

- Roth 401(k)/IRA: Pay taxes now, tax-free withdrawals later

At 60, consider:

- If currently in high tax bracket: traditional contributions

- If currently in low bracket: Roth contributions

- Diversify with both for tax flexibility

Required Minimum Distributions (RMDs):

- Start at age 73 for traditional accounts

- Can create unexpected tax burden

- Plan withdrawal strategy now

Tax-efficient withdrawal strategy:

- Taxable accounts first (usually lowest tax impact)

- Traditional tax-deferred accounts

- Roth accounts last (maximize tax-free growth)

Technology Tools That Help

Budgeting and Tracking

Recommended apps:

- YNAB (You Need A Budget) – zero-based budgeting

- Mint – free expense tracking

- Personal Capital – investment tracking

- EveryDollar – simple envelope budgeting

Investment Management

Robo-advisors for low-cost investing:

- Vanguard Digital Advisor (0.15% fee)

- Fidelity Go (0% fee under $25k)

- Schwab Intelligent Portfolios (no advisory fee)

Social Security Planning

Free calculators:

- SSA.gov – official benefits estimator

- AARP Social Security Calculator

- OpenSocialSecurity.com – claiming optimization

Building Your Support System

Who Should Be On Your Team

Essential members:

- Financial advisor – overall strategy

- Tax professional – minimize tax burden

- Estate attorney – will, powers of attorney

- Insurance agent – proper coverage

- Accountability partner – keep you on track

Free support resources:

- Local Area Agency on Aging

- AARP programs and workshops

- Online communities (Reddit r/personalfinance, Bogleheads forum)

- Local financial literacy programs

Estate Planning Essentials

Documents You Need Now

Even with limited assets, these are critical:

- Last Will and Testament

- Who gets what

- Guardian for dependents

- Executor designation

- Power of Attorney (Financial)

- Who manages finances if you’re incapacitated

- Immediate or springing

- Healthcare Power of Attorney

- Medical decision maker

- HIPAA authorization

- Living Will/Advance Directive

- End-of-life care preferences

- Do not resuscitate orders

- Beneficiary Designations

- Review all accounts

- Update after major life changes

Many of these can be done affordably through online services like LegalZoom or Nolo, though complex situations warrant an attorney.

Your Month-by-Month Action Plan

Month 1: Assessment

- Track every expense

- List all assets and debts

- Calculate net worth

- Estimate Social Security benefits

- Set up free credit monitoring

Month 2: Strategy

- Create zero-based budget

- Identify expense cuts

- Research higher-paying jobs

- Open retirement accounts

- Start emergency fund with $1,000

Month 3: Implementation

- Apply for better jobs

- Start side income pursuit

- Make first retirement contributions

- Reduce one major expense category

- Schedule financial advisor consultation

Months 4-6: Acceleration

- Increase retirement contributions

- Build emergency fund to $2,500

- Negotiate raise or find new job

- Audit and reduce subscriptions

- Review insurance coverage

Months 7-12: Optimization

- Max out catch-up contributions if possible

- Emergency fund to 3 months expenses

- Establish secondary income source

- Consider housing strategy

- Meet with tax professional

When Traditional Retirement Isn’t Possible

Redefining Retirement

For some, traditional retirement simply won’t be financially viable. That’s okay. The goal shifts from “full retirement” to “work optional” or “sustainable semi-retirement.”

Alternative retirement models:

Encore Career:

- Transition to meaningful, less stressful work

- Often nonprofit or community-focused

- Lower pay but higher satisfaction

- Maintains social connections

Phased Retirement:

- Gradually reduce hours

- Maintain some income

- Ease into retirement lifestyle

- Keep active and engaged

Geographic Arbitrage:

- Move to much lower cost area

- Stretch Social Security further

- Consider international destinations

- Popular spots: Portugal, Mexico, Costa Rica, Panama

Staying Motivated for the Long Haul

Making It Sustainable

Recovery at 60 isn’t a sprint—it’s a decade-long marathon. Here’s how to maintain momentum:

Weekly practices:

- Review budget and spending

- Track net worth progress

- Celebrate small wins

- Connect with accountability partner

- Read one financial article

Monthly practices:

- Reconcile all accounts

- Review and adjust budget

- Update written goals

- Assess side income opportunities

- Practice gratitude

Quarterly practices:

- Meet with financial advisor

- Review investment allocation

- Assess progress toward goals

- Update retirement projections

- Reward yourself (within budget!)

Annual practices:

- Comprehensive financial review

- Update estate documents

- Review insurance coverage

- Reassess Social Security strategy

- Plan next year’s goals

The Power of Mindset

Abundance vs. Scarcity Thinking

Your mindset profoundly affects financial outcomes. Research shows that people with abundance mindsets save more and make better financial decisions.

Scarcity mindset:

- “I’ll never have enough”

- “It’s too late for me”

- “I can’t afford that”

Abundance mindset:

- “I’m building security every day”

- “I have time to improve my situation”

- “How can I afford that?”

This isn’t toxic positivity—it’s strategic optimism based on action.

Resource: Which two habits are most important for building wealth

Frequently Asked Questions

Is $100,000 enough to retire at 60?

$100,000 alone is not sufficient for full retirement. However, combined with maxed Social Security benefits ($3,000+/month), reduced housing costs, and part-time work, you can create a viable retirement. Focus on keeping expenses below $3,000-3,500 monthly.

Should I tap my home equity?

Only as a last resort. Your home provides:

- Housing stability

- Downsizing option later

- Inheritance for heirs

- Reverse mortgage option (final resort)

Better options: downsize to smaller home, rent out rooms, relocate to cheaper area.

Can I retire with just Social Security?

Millions of Americans do, but it requires extreme budgeting. The average benefit of $2,000/month means keeping total expenses under this amount. Feasible in low cost-of-living areas with paid-off housing.

Should I claim Social Security at 62?

Almost never. Unless you have serious health issues or absolutely no income options, delaying increases your lifetime income significantly. Every year you wait adds 8% to your benefit.

Is it better to pay off debt or save for retirement?

Attack high-interest debt (20%+) aggressively while making minimum retirement contributions. For low-interest debt (5% or less), prioritize retirement savings with catch-up contributions.

Your Next Steps Right Now

Don’t let this be another article you read and forget. Take these three immediate actions:

Action 1: Track Your Spending (Today)

Download a budgeting app or create a simple spreadsheet. Starting today, record every single expense for the next 60 days. You cannot change what you don’t measure.

Action 2: Check Your Social Security (This Week)

Create an account at SSA.gov/myaccount. Review your earnings history and estimated benefits. This takes 15 minutes and provides critical planning information.

Action 3: Open a Retirement Account (This Month)

If you don’t have one, open a Roth IRA at Vanguard, Fidelity, or Schwab. Start with whatever you can—even $50. The psychological impact of taking action is powerful.

Conclusion: Your Path Forward

Being 60 with no retirement savings feels overwhelming. The shame is real. The fear is valid. But giving up is not an option.

You have approximately 10-15 working years ahead of you. During that time, you can:

- Build $100,000-300,000 in retirement savings through aggressive saving

- Maximize Social Security benefits through strategic delayed claiming

- Reduce housing costs significantly through downsizing or relocation

- Establish secondary income sources that continue into retirement

- Create a sustainable budget that works for your situation

Will you have a lavish retirement? Probably not. But with strategic action starting today, you can absolutely achieve financial security and dignity in your later years.

The choice is yours: continue down the path of anxiety and inaction, or take control starting right now. Thousands of people in your exact situation have successfully recovered. You can too.

Remember: The best time to start was 30 years ago. The second-best time is today.

Take Action Today

Ready to transform your financial future? Here’s your immediate action checklist:

Week 1: Download budgeting app and start tracking expenses. Create SSA.gov account and review benefits List all assets, debts, and income sources. Calculate current net worth. Set up emergency fund with initial $50-100

Week 2: Research higher-paying job opportunities. Update resume and LinkedIn profile. Apply to 3-5 better positions .Identify one immediate expense to cut. Open retirement account (IRA or 401k)

Week 3: Schedule meeting with HR about 401k options. Research side income opportunities. Contact Area Agency on Aging for resources. Audit all subscription services. Create written 10-year plan

Week 4: Make first retirement account contribution. Build emergency fund to $1,000. Schedule financial advisor consultation. Join online personal finance community. Review and celebrate progress

The journey of financial recovery starts with a single step. Take yours today.

Disclaimer: This article provides general financial information and education. It is not personalized financial advice. Consult with qualified financial, tax, and legal professionals about your specific situation.

Karthick Raja, MBA, is a personal finance educator and HR professional with 10+ years of experience in Personal Finance ,taxation, payroll, and career development. He helps readers build wealth, manage money wisely, and grow professionally.